Faston

Commodity

& Business

Advisor AB

Insights and Articles

Share our thoughts

Hockey sticks Synthetics

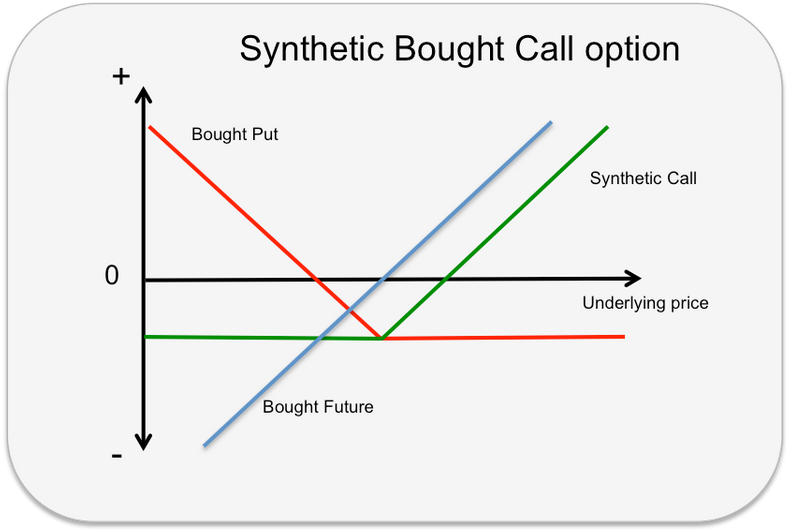

Synthetic Call option

By combining an option and the underlying it is possible to replicate payouts of other options, so called synthetics.

To build a synthetic bought call options position, you buy a put option (red) and a future (blue). In this example, the put option is an at the money at the time the future is bought. The future is crossing the breakeven level (the black line) at the market price. The positive payout from the put option is netted by negative payout from the futures in a market that falls below the strike price. In this case there will be no return that covers the cost of the premium, which will be constant regardless of how low the market goes. On the other hand if the market increases the payout from the future will create positive return. The put option does not net this gain. The only cost left is the premium paid in the beginning and overall the payout properties will resemble the one of a bought call the green line. You buy volatility by buying the option and you by the direction by buying the future.

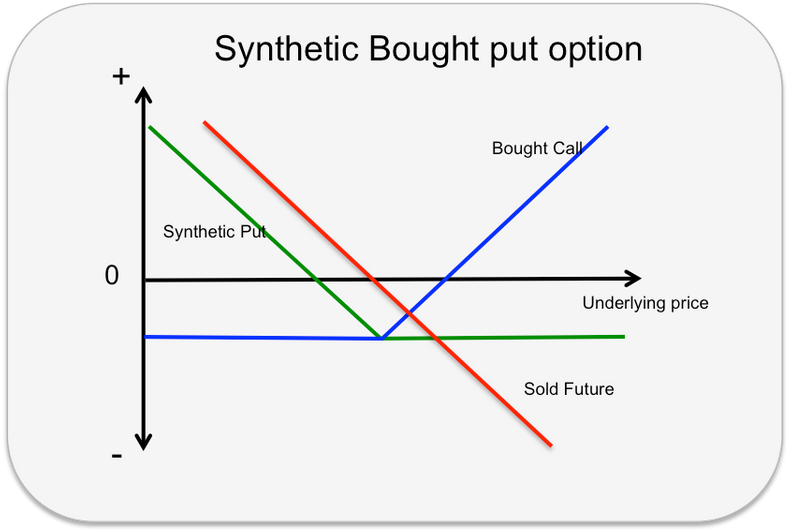

Synthetic put option

To build a synthetic put option you buy a call option and sell a future. The future gives a positive return in a falling market and a loss in a rising market. The loss is netted by the positive return from the call option with the premium of the option as the remaining cost.

About Us

Contact

Insight

Home

CONNECT WITH US

Follow Us On Social Networks

Faston

Commodity

& business

advisor

Copyright © Faston 2016